It was another “good news is bad news” trade with better-than-expected labor market reports boosting fears over a higher for longer stance from the FOMC. Hawkish Fedspeak added to the selloffs in stocks and bonds but supported the Dollar. Wall Street closed over -1.0% in the red and just off the day’s lows. Treasury yields spiked, led by the front end as the curve inverted further to -74.2 bps versus -67.2 bps Wednesday and the most since December 15. Tweaks in Fed policy outlooks remain a major driver for the markets, as heading into the key nonfarm payroll report today.

- The USD Index jumped above 105.00 and holds.

- EUR – back to 1.0500 bottom. German manufacturing orders plunged -5.3% m/m in November. German retail sales rose 1.1% m/m in November, less than hoped in light of the Black Friday sales, which are a relatively new phenomenon in Germany.

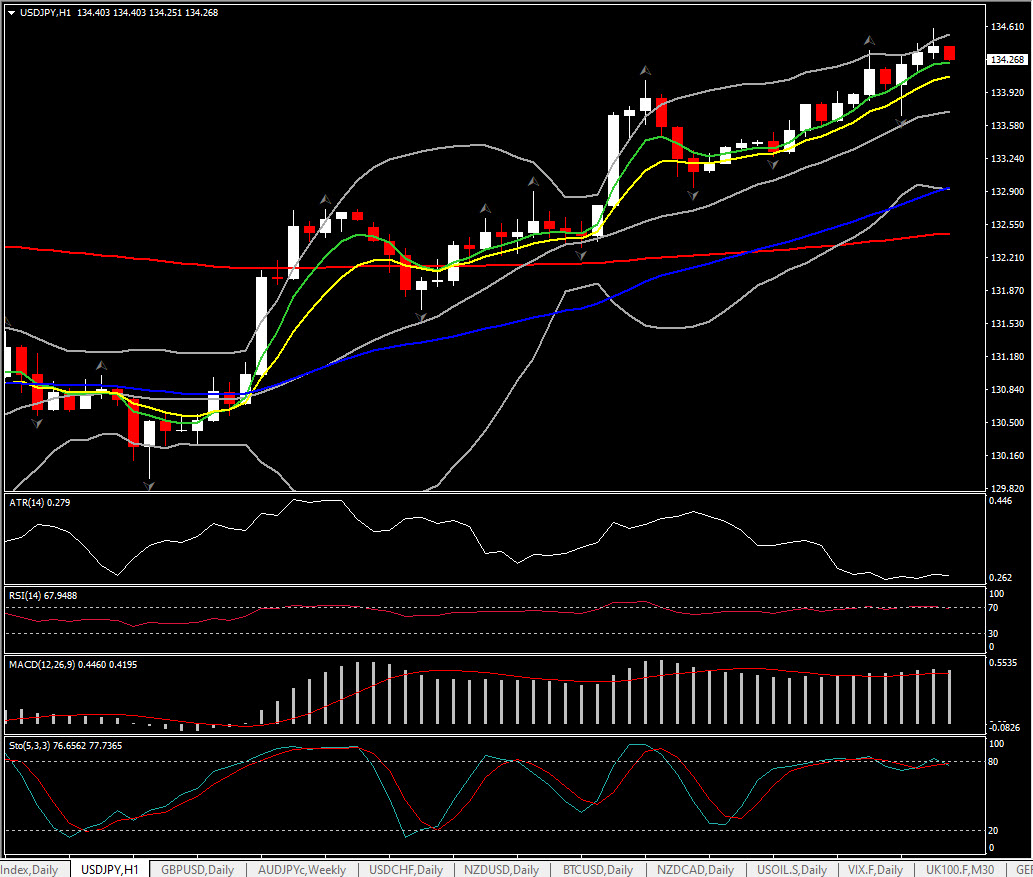

- JPY – has lifted to 134.20.

- GBP – under pressure to 1.1890.

- Stocks – The US100 dropped by -1.42%, with the US500 -1.16% and the US30 off -1.02%. Nearly all the S&P 500 sectors were in the red with the exception of energy. AAPL -1.06%, MSFT -2.96% & AMZN -2.37%.

- USOil – stuck at $73.80. Virus developments remained in focus and there is still speculation that China will add further support measures as the economy tries to cope with the impact of rising Covid-19 case numbers.

- Gold – extended lower at $1832, after Putin ordered a holiday ceasefire in Ukraine from January 6-7. Bullion has fallen from an overnight peak of $1859.04.

Today: Markets are now waiting for US payroll numbers and Eurozone inflation data, which are hoped to give further indications on the monetary policy path on both sides of the Atlantic.

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.73%). Above 134.00. MAs aligned higher, MACD histogram & signal line positive and rising. RSI 71 & neutral, H1 ATR 0.272, Daily ATR 1866.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.