The first full day of 2023 saw stocks flat, a bid for the Greenback & Yen, weaker EUR following softer German CPI data and Oil markets collapse on global growth worries. Treasuries are firmer with US10yr yields losing -2.61%. Overnight Asian stocks have traded mostly firmer despite the negative handover from Wall Street; Hang Seng outperformed whilst Nikkei lagged (-1.45%). AUD outperforms. “China pledges ‘final victory’ over COVID as outbreak raises global alarm” – RTS lead story.

- The USD Index rallied to 104.50 yesterday as the USD got a significant New Year bid in early European trades on increased volumes. Softer at 104.10 now.

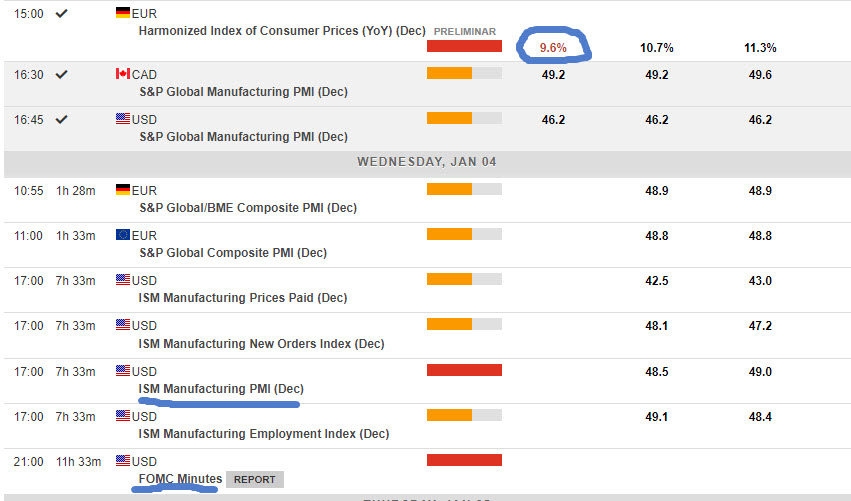

- EUR – tanked to test 1.0520 after the German CPI and USD bid, back to 1.0580 now.

- JPY – hit new 7-mth lows under 130.00 at 129.50 on Tuesday before recovering to 131.40 highs today and trades at 130.40 now.

- GBP – Sterling sank to 1.1900 as USD rallied before recovering to the key 1.2000 today.

- Stocks – The US markets closed down (-0.40-0.76%). US500 -15.36 (-0.40%) at 3824 #TSLA -12.24% the worst performer. #APPL fell -3.74% and its market cap is now below $2 trillion level. XOM & CVX hit from a -4% collapse in Oil prices. US500.F trades at 3853 now.

- USOil – Tanked from $81.50 highs in early trades yesterday over 4% its biggest 1-day fall in over 3 mths on global demand concerns and China Covid cases. Trades at $76.45 now.

- Gold – Has taken another leg higher today on USD weakness, continued CB rate hikes and subdued economic outlook. Breached $1830 in early trades, is over the next resistance at $1850 and trades at $1858 now.

- BTC – Sentiment woes continue – the biggest coin trades at $16.8k today. Sam Bankman-Fried pleads not guilty in FTX fraud case; October trial set.

Today – German Import Prices, Swiss CPI, EZ Services and Composite Final PMIs, US ISM Manufacturing PMI, FOMC Minutes, Crude Private Inventories.

Biggest FX Mover @ (07:30 GMT) AUDUSD (+1.08%). A volatile day yesterday took the pair down to under 0.6700 and today its has tested all the way back to 0.6850. MAs aligned higher, MACD histogram & signal line positive and rising. RSI 72.30 OB and still rising, H1 ATR 0.00198, Daily ATR 0.0091.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.