FOMC, Dollar, S&P 500, ECB and BOE Rate Decision Talking Points:

- The Federal Reserve hiked its benchmark rate 25bps to a range of 4.50 – 4.75 percent

- The US benchmark is higher than its principal global counterparts, but that advantage has been previously priced in

- In the policy statement that accompanied the decision, the group said ‘anticipates that ongoing increases…will be appropriate’

Recommended by John Kicklighter

Trading Forex News: The Strategy

The Federal Open Market Committee (FOMC) announced a 25 basis point increase in its benchmark rate range to 4.50 – 4.75 percent. The increase was a further step down in pace from the 50 bp increase in December and the 75 bp hike in November – following a stretch of four consecutive such heavy hikes. The increase in the benchmark rate was in-line with the consensus forecast from economists and the market itself via Fed Fund futures, so it was perhaps not a surprise that the initial market response centered on volatility without a clear view on direction.

With the market’s looking for clues to the Federal Reserve’s ultimate top for its benchmark lending rate, the monetary policy report offered some conflicting signals. On the one hand, the group mentioned that inflation had ‘eased somewhat but remains elevated’ – removing the references to volatile energy and food components. The maintenance of the remark that the group “anticipates that ongoing increases in the target range will be appropriate in order to…return inflation to 2 percent” is an unexpected hawkish perspective.

Some of the highlights from Fed Chairman Jerome Powell’s press conference following the rate decision include:

Hawkish Overtone

- The discussion is around ‘a couple more rate hikes to get to appropriately restrictive stance’

- FOMC will make decision on a meeting-by-meeting basis

- Full effects of the rapid tightening cycle has yet to be fully felt

- Suggests they are discussing a couple hikes to get to more restrictive stance

- Taking pauses between meetings was not discussed

- If the economy performs as expected, doesn’t expect a rate cut in 2023

Dovish Overtone

- Says the Fed will need to stay restrictive for some time

- Will need more evidence of inflation pressures weakening to be confident it is under control

- Will likely need to maintain a restrictive policy stance for some time

- Encouraging to see the ‘deflationary process has started’

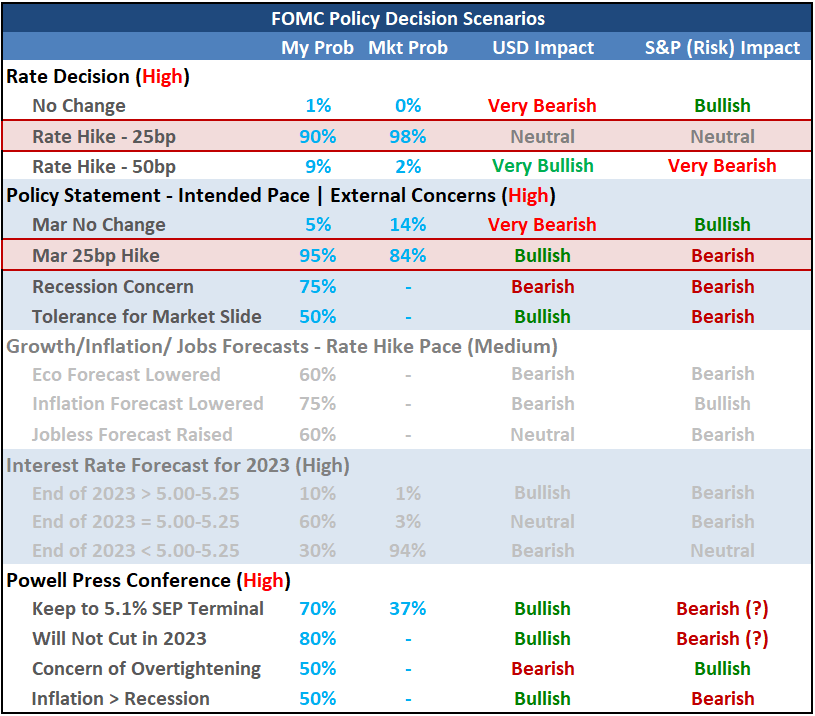

FOMC Scenario Table

Table Made by John Kicklighter

Looking to the intraday chart of the active S&P 500 emini futures contract, the initial response to the FOMC hike was a drop which aligns to risk aversion that tends to draw on the market’s speculative connection to monetary policy as a backstop for risk exposure. However, that decline was sharply reversed without hitting any critical technical levels as investors looking for greater clarification on the path forward.Ultimately, through both hawkish and dovish remarks from the head of the Federal Reserve, the equity market drew upon the more supportive remarks pushing the S&P 500 to its highest levels since September above 4,100.

Chart of S&P 500 Emini Futures with Volume (5-Minute)

Chart Created on Tradingview Platform

With a connection to risk trends as a safe haven as well as its relative potential via yield differentials, the US Dollar would dive during Chairman Powell’s remarks. Ultimately, the US yield is a premium to most counterparts and the Greenback has reversed more than half of its run up through 2021-2022 – rooted heavily in the anticipation of that yield advantage – yet that doesn’t seem to be enough of a rebalancing for the US currency.

Chart of the DXY Dollar Index (5-Minute)

Chart Created on Tradingview Platform

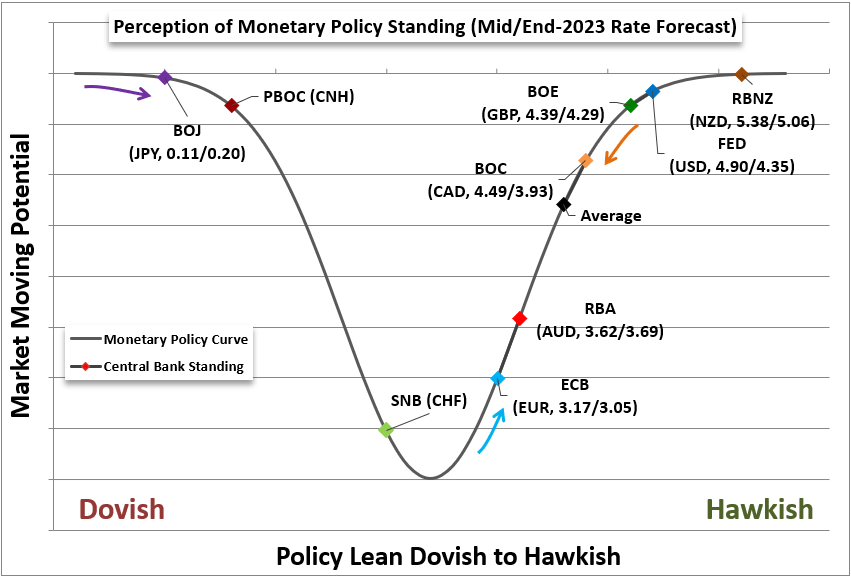

While the Federal Reserve’s and market’s outlook for the terminal rate and the path through the end of 2023, the US benchmark is still seen to sport a premium in the rate differential against most its major counterparts – and specifically the most liquid counterparts. Fed Fund futures are pricing in a 4.90 percent rate through the June contract, which is a premium to the three largest counterparts: ECB (3.17), the BOE (4.39) and of course the BOJ (0.11).

Table of Relative Monetary Policy Standing

Table Made by John Kicklighter

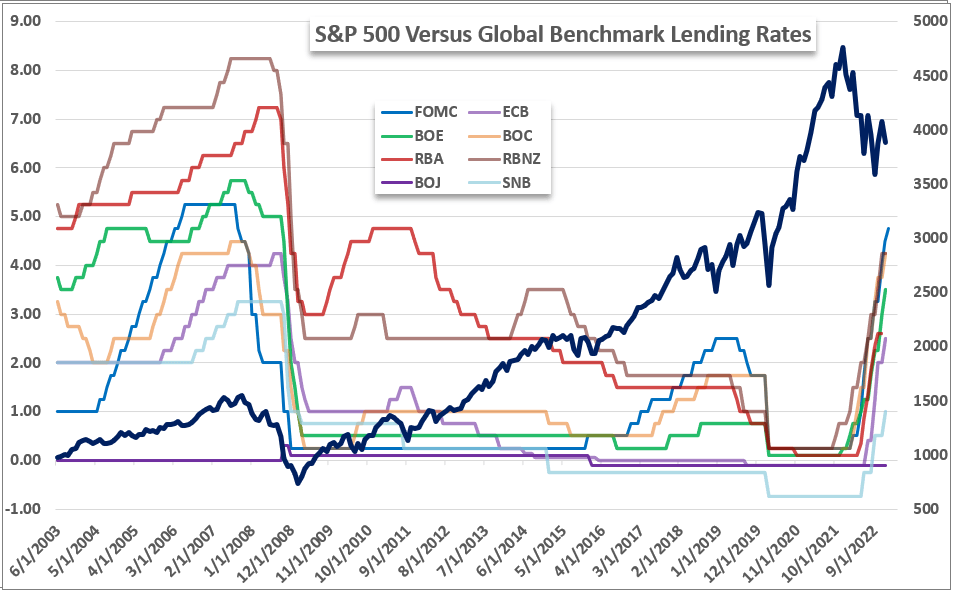

Taking a bigger picture look at monetary policy rates across the globe, it is important to remember where the Fed sits in the global spectrum. It is a leader of an exceptional tightening regime that has thus far had a fairly measured impact on the financial market: below represented by the S&P 500. If the tighter conditions lead to a recession, the second round effect on investor confidence should not be missed as a by-product of monetary policy.

Table of Relative Monetary Policy Standing

Table Made by John Kicklighter